- Stochastic Process course notes

1. Definition

- Probability function: $f(x) = \lambda e^{-\lambda x}$, $x \geq 0$

- Cumulative Distribution Function (CDF): $F(x) = 1-e^{-\lambda x}$, $x \geq 0$

- Complement of the CDF (CCDF): $F^c(x) = e^{-\lambda x}$, $x \geq 0$.

2. Memoryless Property

Def`1: A random variable X has the memoryless property if $Pr\{X>t+s| X>s\} = Pr\{X>t\}$

Def`2: A random variable X has the memoryless property if $Pr\{X>t+s\} = Pr\{X>t\} Pr\{X>s\}$

The exponential distribution is the only distribution that has the memoryless property (Satisfy definition 2)

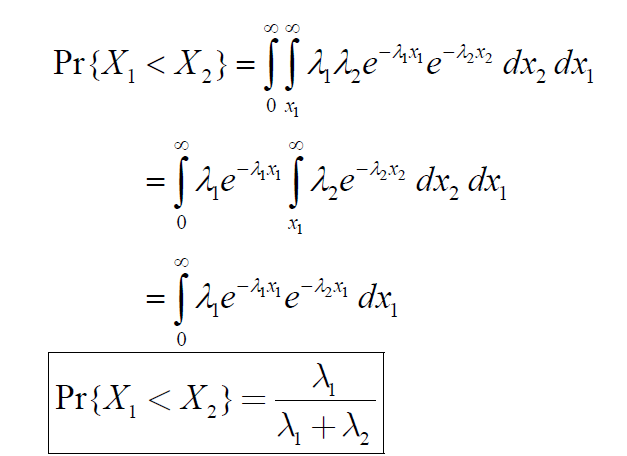

Then what is the probability that $X_1 < X_2$.

More generally

$Pr\{X_i = min[X_1,\cdots, X_n]\} = \frac{\lambda_i}{\lambda_1+\lambda_2+\cdots +\lambda_n}$

Def`2: A random variable X has the memoryless property if $Pr\{X>t+s\} = Pr\{X>t\} Pr\{X>s\}$

The exponential distribution is the only distribution that has the memoryless property (Satisfy definition 2)

3. Useful Properties: First occurrence among events

Assume $X_1, X_2, \cdots, X_n$ are exponential variable with rate $\lambda_1, \lambda_2, \cdots, \lambda_n$.Then what is the probability that $X_1 < X_2$.

More generally

$Pr\{X_i = min[X_1,\cdots, X_n]\} = \frac{\lambda_i}{\lambda_1+\lambda_2+\cdots +\lambda_n}$

4. Distribution of time of first event

This is the CDF of an exponential RV with rate $(\lambda_1 + \lambda_2)$, therefore

$min(X_1, X_2)$ ~ $exp(\lambda_1 + \lambda_2)$

5. Distribution of time of last event (maximum)

No comments:

Post a Comment